When traveling, you naturally want to get the best exchange rate, so that your money goes further – which is especially important given how the USD has been steadily weakening. This article will tell you exactly how to get the best exchange rates while overseas.

1) Find out if your current bank has a partnership with any overseas bank. For example, Bank of America has a partnership with WestPac in the Australia region. If you use your existing bank card with a partnered bank, you not pay zero bank fees, but you also get favorable exchange rates!

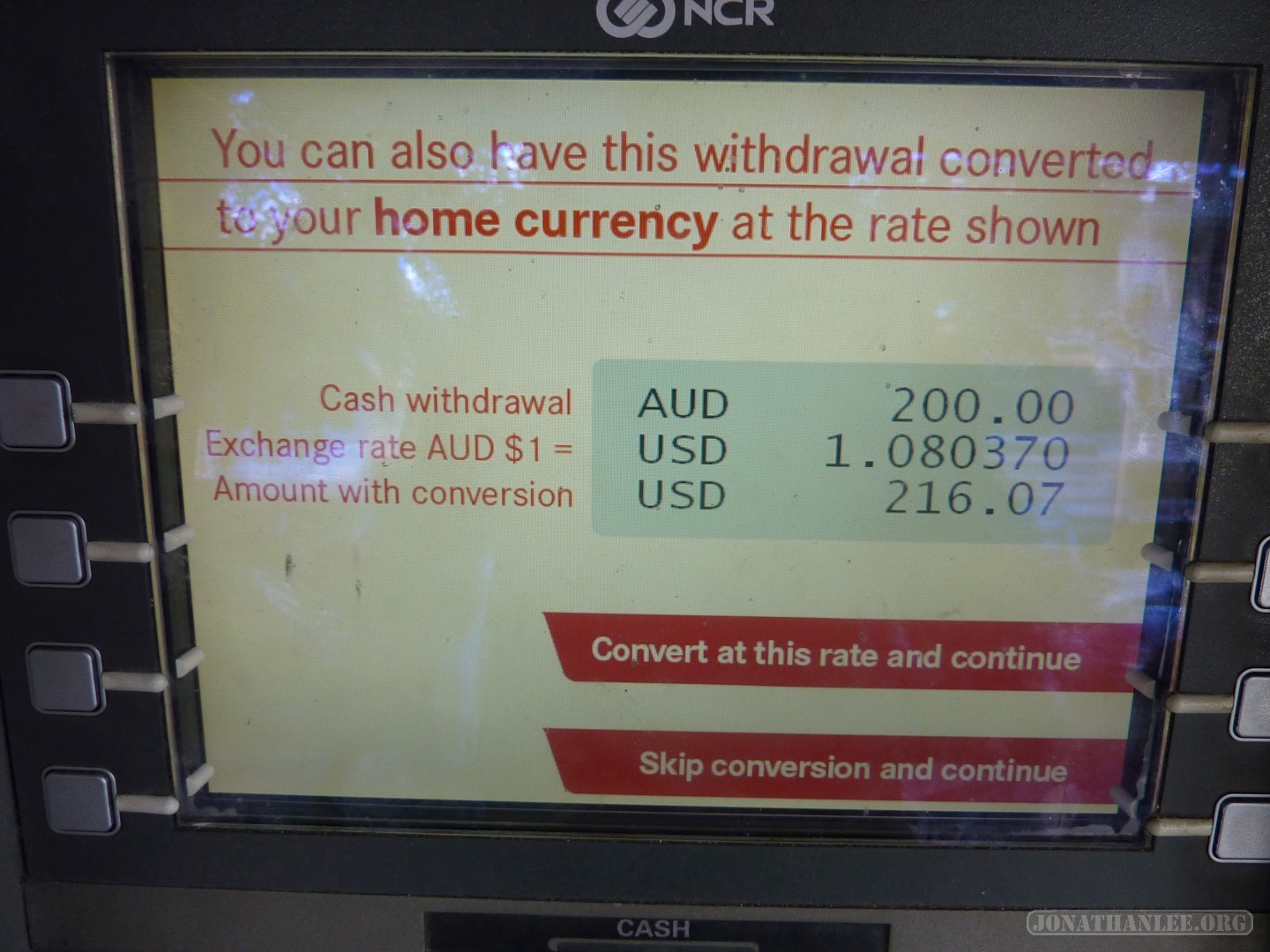

It’s important to note, the partner bank may offer to convert your withdrawal into your home currency at it’s cash “buy” rate, as shown below. Note how this dialogue box is intentionally ambiguous, not telling you what will happen if you skip conversion. But don’t do it! If you skip conversion here, it will be automatically converted at a much better rate (the Visa daily rate).

No, skip conversion at this horrible rate! (VISA rates were at ~1.04 at this time)

2) Open a brokerage account with Charles Schwab, and you will automatically receive a Charles Schwab Checking account and accompanying debit card. Use this debit card to withdraw money at any ATM. You will have to pay a bank fee, but Charles Schwab will refund that money to you at the end of each month.

Using either option 1 or option 2, you will exchange money at the daily Visa rate.

3) Use a credit card. Depending on your card, you will have to pay a foreign exchange fee around 3%. There are special cards that charge no foreign exchange fee, but I find that not only is it a hassle to apply, but there are often annual fees.

4) Bring USD, and use a money changer in the city. You will have to pay a foreign exchange fee (spread) of around 5%. From personal experience, I have found that small exchange kiosks (foreign exchange businesses) usually offer better rates than big banks.

Here’s an example of some pretty bad exchange rates being offered by a bank:

5) Bring USD, and use a money exchanger at the airport. Foreign exchange fee of around 8%. Ouch!

6) Use your regular ATM / debit card at a non-affiliated bank. You will typically get charged a $2-$10 bank fee. If you don’t like carrying too much cash, and make many small withdrawals, these add up very quickly!

For a demonstration, you can check out the numbers in this real-life example:

| Date | Service | Charge AUD | Amount USD | Fee USD | Stated Rate | Effective Rate | Daily Visa Rate | Difference | |

| 3/6/2013 | Amex | 36 | 36.91 | 0.99 | 1.02527778 | 1.052777778 | 1.02677 | 0.026008 | |

| 3/6/2013 | Schwab ANZ | 102* | 104.72 | 1.02666667 | 1.026666667 | 1.02677 | -0.0001 | ||

| 3/8/2013 | BoA Visa | 71 | 73.08 | 2.19 | 1.02929577 | 1.060140845 | 1.02933 | 0.030811 | |

| 3/11/2013 | BoA Westpac | 100 | 102.11 | 1.0211 | 1.0211 | 1.02876 | -0.00766 | ||

| 3/11/2013 | BoA Westpac | 100 | 102.11 | 1.0211 | 1.0211 | 1.02876 | -0.00766 | ||

| 3/13/2013 | BoA Westpac | 200 | 205.52 | 1.0276 | 1.0276 | 1.03396 | -0.00636 |

* I withdrew $100, and was charged a $2 bank fee, but Charles Schwab refunded it at the end of the month.

As you can see, I paid the lowest exchange rates when using options 1 and 2 – using my existing bank card at a partnered bank, and using my Charles Schwab debit card.

Other travel websites often give alternate ‘expert’ advice that is often more trouble than it’s worth

– Traveler’s check: These tools are useful, but you often have to pay a fee to get your bank to provide the check.. In a world where ATMs are everywhere, if you can withdraw money without paying ATM fees, traveler’s checks are outdated.

– Services that “deliver” foreign currency to you while overseas: you can get good exchange rates with these services, but they are a tremendous hassle, since you have to book well in advance. I prefer the flexibility of being able to find an ATM anywhere. This option may be useful if you need access to very large amounts of money.